As Climate Investing Shifts to Adaptation, Water is Taking Stage

Adaptation and resilience are emerging as the central themes in climate investing, with water in the lead. Once overlooked as fragmented, slow, and undervalued, a changed climate is making water impossible to ignore.

Decarbonization has been at the forefront of climate investing for good reason - the climate crisis demands a concerted effort on mitigation. Throughout it all, water has stayed in the background, despite its clear ties with climate, many intersections and parallels with energy, and despite water arguably being the hardest of all the hard-to-abate sectors. Water has never really been a part of the mainstream climate conversation, other than in an acknowledgement from time to time.

The times, they are a-changin’. Specifically, the hydrological cycle is changing. Rainfall patterns are changing. Droughts and floods are on the rise, causing loss of property and life. We are fundamentally altering the predicate of much of our lives - from where we live and work to where we grow food.

McKinsey projects that by 2030, demand for water will outstrip supply by 40%. Today, about half of humanity experiences severe water scarcity for at least part of each year. Water-related hazards are accelerating - since 2000, flood disasters have increased by more than 134% and droughts have become 29% longer. The increase in intensity of droughts and floods is on a trendline that’s scary. The link between climate and water is now obvious and undeniable. Climate and water are inseparable: climate change is making water scarcer, more unpredictable, and more polluted. Climate change is water change.

Water is the fundamental resource for the planet, all life, and the economy. While the $1.6 T/yr water sector is only about 1.5% of global GDP, it underpins about 60% of global GDP - and water is at the bottom of Maslow’s hierarchy of needs. What good is more important than water?

When water is abundant and unpolluted, all is good - we take this invaluable resource for granted. With the implementation of centralized water & wastewater treatment plants and pipe networks after the turn of the last century, and then the adoption of the Clean Water Act and related policies around the world to control pollution, water has been, for the most part, pleasantly in the background. The most fundamental molecule of them all has just been there for us, blissfully.

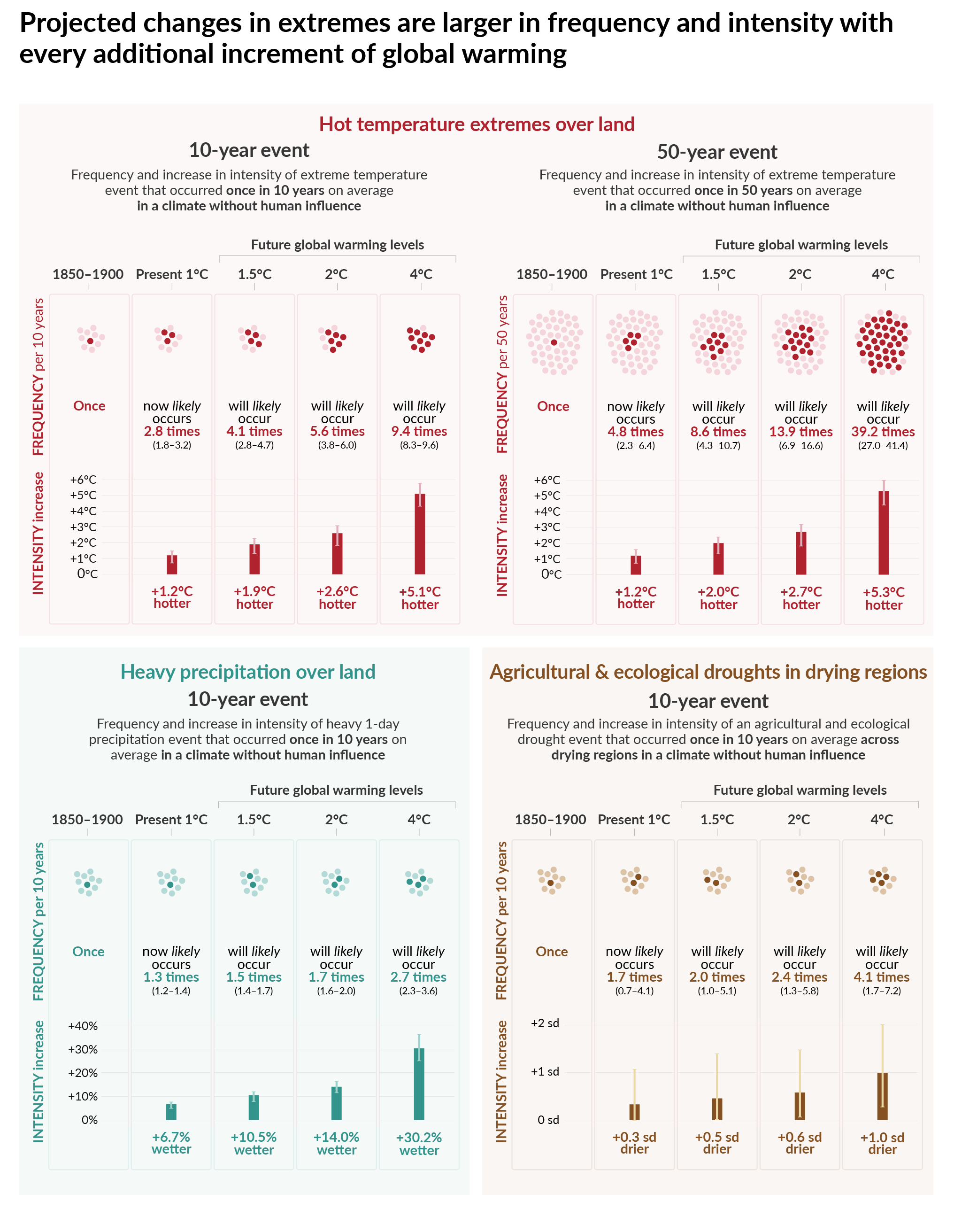

The IPCC’s sixth assessment report (AR6) details the effects of warming on droughts and floods, clearly showing that as the planet warms further that both the frequency and the intensity of droughts and floods increase - as a consequence of the changing hydrological cycle. We’re experiencing it now, and it’s going to get worse.

{kind=link}

The Planet is Warming - But Decarbonization is Losing Steam

The world had firm commitments to achieve Net Zero emissions by 2050 and stave off the worst of climate change. Nearly every country is party to the legally binding 2015 Paris Agreement, though the US initiated its withdrawal on January 20th to join Iran, Libya, and Yemen on the sidelines. The countries in the accord have committed to limit average planetary warming to 2 oC over pre-industrial times, and preferably to just 1.5 oC. The pace of achieving those commitments is too slow - many decarbonization plans by countries and companies are back-end loaded. Carbon mitigation is not happening as was hoped for, or as needed. The problem is that the effects of climate change get accentuated as decarbonization gets off track.

NASA says that in 2024, the earth was 1.47 oC warmer than the pre-industrial benchmark, and if current global decarbonization policies are achieved, it’s projected that the planet will warm to 2.7 oC - and based on our track record, that’s probably optimistic.

This shift away from renewables and decarbonization has taken some wind out of the sails of climate mitigation - but is catalyzing interest and investment in climate adaptation and resilience as hard realities set in. The world can choose to delay decarbonization, but it cannot avoid the impacts of a changed climate. There’s no avoiding reality when the rivers run dry, when floods hit, or when wildfires rage.

The decarbonization pullback means the impacts of climate change are accelerating - with the hydrological cycle, and the water sector, feeling the brunt of this change. The shift away from Net Zero is causing disruption in water, necessitating investment in the sector and attracting entrepreneurial energy to the challenge.

How Does Climate Change Impact Water?

The impacts of climate change on water are wide-ranging and profound:.

Water scarcity:

Water scarcity reduces freshwater availability to communities, agriculture, and industry. The canary in the coal mine was in Perth, Australia, where rainfall has dramatically decreased over the past few decades, causing nearly a total shift away from surface water to seawater desalination, water reuse, and groundwater replenishment. Many other regions are now experiencing a similar change - a lack of rain when they used to have it. As Fuller said in the 16th Century, “We never know the worth of water till the well is dry.” True then, and true now.

A first reaction is to pump water from aquifers, but that’s not sustainable, and we’re seeing groundwater decline and depletion, land subsidence, and saltwater intrusion. Groundwater abstraction is more of a determinant of sea level rise than melting glaciers.

The public is getting concerned, and protective, about their water supplies, as we recently saw in Tucson where public opposition to a water thirsty data center led to the project being shuttered, despite its employment and economic benefits. The $17bn “Project Sail” datacenter in Georgia is seeing similar headwinds.

Extreme rain events:

69% of the impacts of climate change are now expressed through water. The number of billion dollar losses is rising exponentially and we’ve all seen the horrifying potential for death and destruction from flooding.

More frequent and more intense urban rainfall stresses stormwater infrastructure and is inducing migration away from areas prone to flooding.

And a host of other effects, including:

A warming planet is accelerating the occurrence of harmful algae blooms (HABs) in surface waters, which produce toxins and reduce oxygen levels, contaminating drinking water supplies and killing aquatic life.

Warmer temperatures mean increased evaporation and transpiration and higher water consumption in agriculture.

Increased transpiration rates lead to an increase in local air temperature, which in turn creates a positive feedback loop.

Climate change accelerates the degradation of water infrastructure.

As a consequence, investment in water can only accelerate and become a multi-decade megatrend. There is no other outcome; we have no choice. Smart capital allocators are already acting, and we’re seeing the exit environment take shape. The rates that water and wastewater utilities charge their citizens, which is a direct consequence of the investment in infrastructure being made, are rising - the last global tariff survey by Global Water Intelligence showed that rates increased YoY globally by 10.7%. This is only the start.

Energy & Water Are Similar - And Different

Water and energy have an inextricable linkage and interdependency - they are both needed to run the bulk of the world’s economy and support society - they are both deeply important sector verticals and horizontals. But unlike electricity, which is weightless and can be transmitted vast distances through wires, water is heavy and is more difficult to move, making water a particularly local issue.

The challenges, and solutions, in water have many parallels with energy:

Efficiency is often the best first move in energy, and the same is true in water.

When water is plentiful and cheap, there’s little concern about waste, but when it’s scarce, the results from efficiency programs are impressive. Prior to Cape Town’s “Day Zero” water crisis in 2017-2018, water consumption was at about 183 liters/person/d and afterwards it dropped to 84 l/p/d, and was as low as 50 l/p/d during the crisis. What’s the average water use in the US? It’s 310 l/p/d - we have room to improve.

The proportion of drinking water that utilities put in pipes that they don’t get paid for, called “non-revenue water”, is around 30% on average globally, and much higher in many places. In regions that put an effort to fix the leaks and other issues, the loss rate is < 5%.

Whereas solar, wind, and geothermal have provided new sources of energy generation, desalination, reuse, aquifer replenishment, and atmospheric water generation are providing new sources of water.

Seawater desalination is booming in the Middle East, but permitting and other issues are making costs high in the West (innovators are developing new solutions to address).

The water industry is rallying around the percent of water that’s reused as the sector’s CO2 metric - and for good reason. Despite the “yuk” factor that thankfully we’re progressing past, treated water from reuse systems is higher quality than drinking water produced from typical sources and, if you think about it, all water is reused.

California just extended their Title 22 reuse regulations to include Direct Potable Reuse (DPR), leading to a rush by technology providers and engineering firms to provide the solutions. And, just like California led in solar and wind regulations, Title 22’s DPR regulations are being looked at as a model for direct potable reuse elsewhere.

Only about 8% of freshwater withdrawals are reused. The industry is beginning to rally around a 50% reuse target, but will need to define protocols and means for tracking.

The investment tax credit (ITC) was instrumental in helping to scale the renewables industry, particularly solar. There is now draft legislation, the Advancing Water Reuse Act (H.R. 2940), to establish an ITC for water reuse systems.

Digitization, software and AI have helped with the optimization and use of energy and energy systems, they are doing the same in water.

Come Test the Waters

Water is an easy adjacency for climate, sustainability, circularity, and decarbonization investors. We’ve had the pleasure of co-investing with many top climate VCs as well as VCs that are more climate agnostic - the fundamentals that make water an attractive segment for investment are there, whether the climate argument is invoked or not.

There are a wide range of investment drivers beyond climate in water, including a plethora of pollutants such as microplastics, PFAS, pharmaceuticals, and algae blooms; water infrastructure is aging - including much of the 2.3 million miles of sewer pipes in the US and Europe; thirsty semiconductor fabs, data centers, and industry; the boom in critical materials and the role of separations tech in advanced mining processes such as DLE as well as in mining brines and even wastewaters; developing country infrastructure needs; and more.

The unfortunate decarbonization pullback is accelerating the need to deal with the reality of climate change. Adaptation will be an inexorable investment theme for the coming decades, and water will play a chief role. The business of managing the tasteless, odorless, wondrous, simple molecule that is the source of all life is gathering commercial momentum. The founders we see across the landscape of the sector are remarkable, and our investment decisions have become very tough indeed. This is what the early days of market inflection look like. We’re rather glad we started when we did, but the next best time to start is today. We’re here if we can help.