The End of the Beginning: Financing in Water is Entering its Growth Era

This is a keynote given by Tom on the main stage of the Innovation Driven Water Sustainability Conference in Jeddah on December 10th.

Good morning everyone, my name is Tom Ferguson and I’m the Managing Partner of Burnt Island Ventures, the water focused venture fund. We’re just approaching $100m AUM, we’ve invested over $60m in 34 companies since early 2021, and we pride ourselves in being at the vanguard of proving that investing at the seed stage in water can be a very profitable undertaking indeed.

I’m aware that there are some contradictions at play here - I’m a Scotsman who sounds English who lives in Brooklyn who started a water-focused venture fund in the US, giving a speech on water finance in Saudi Arabia to people who really understand the value of water. I grew up with endless quantities of it falling out of the sky, so I’m aware our contexts are very different. But I hope you can bear with me because I come bearing good news about early stage water financing.

It’s really a pleasure to be with you this morning to describe a new chapter in the development of water as an investment theme. We’ve called it “The End of the Beginning”, because we think something fundamental shifted this year, and we’re excited to walk you through our logic for why we’re now in a new defined era of water investment. First, I will look at the shift in the early stage market that happened from 2020-2025, that has laid a very promising platform for the future of investment in the sector. Second, I want to take you through the logic of the emergence of a true growth market in water. Third, I will make the case that this is an inevitable, low-risk opportunity because major downstream capital has cottoned onto the water opportunity before the venture world has, which gives rise to some very interesting dynamics indeed.

In the last five years, something has changed in the investment world with regard to water. In 2020, people were still viewing a water fund as a charity or impact investment, corporates were seeing water principally as a CSR risk, or the element of their operations they knew they needed but cared least about. That has fundamentally shifted. Whether it’s through water scarcity, increasing prices, the propagation of data centers, or the financial results of some of the largest water companies, lightbulbs have come on for public and private investors that water is a defensive, foundational, high-growth asset class. There has been the beginnings of a realisation of what is true in our sector: That the tailwinds are inevitable, it is unidirectional, and the numbers involved are enormous – $1.6trn in capex and opex in 2025, growing at at least 8%.

The most important tailwind to water is physical, the distortions happening as a result of global heating. This chart from GWI shows the escalation in excess inundation or drying events worldwide as measured through the gravitational pull of groundwater by NASA. The steadiness we have relied upon in terms of our water cycle increasingly no longer holds true across the world. Variability is so difficult because water, wastewater, stormwater systems have to deal with extremes. And there is no question about the expansion of water’s extremes.

Massive inundation stories, from Texas to the UK to the Philippines to Dubai are becoming so commonplace so as to be easily missed in the global press. Flooding events are up 6x from 2000 with no sign of slowing as the air becomes more saturated with more evaporated water, increasing the ferocity and length of storms and inundation events.

And the converse is also true. Extended drying events are also more commonplace. The drying of Europe, the potential need to relocate Tehran, the subsidence issues in the Central Valley of California. The extremes of the impacts of global heating are placing unprecedented pressure on infrastructure, safety and access.

So this really is a $1.6trn market having a truck driven through it. And the beauty of it as an investment market is its breadth. We’ve just closed our $50m Fund II, and out in the fundraising market, more often than not I hear “nice niche”. Niche? This is FIVE TIMES the size of the SaaS market, and fundamental to all life and every industry on earth, whether they acknowledge it or not. This is colossal, but much more importantly it’s everywhere. From process water and water treatment across oil and gas, mining and metals, dairy, agriculture, to domestic appliances, insurance, metals reclamation, sludge management, desalination, replenishment and yes, of course, data centers. There are just so many water markets riddled with inefficiencies for smart people to come in and build businesses.

And supporting them is our business. At BIV we’re in the business of finding, funding, and supporting the best entrepreneurs in water in the world. We’re here to support the people who are building the vehicles of change, slashing costs, increasing speed, improving outcomes, reducing complexity, reducing environmental impacts.

To know where we are as an early stage financing market, it helps to see the world as I saw it when I started BIV.

I founded this firm because every investable asset class or vertical goes through the same process, whether it’s Fintech, or Proptech, even Cloud SaaS - AI went through a very accelerated version of this. All of them follow a pathway, where there is a period of initiation, and then there is a ton of accelerated progress building on the foundations laid in the initiation phase, and then maturation, where you level off into a known, understood, and trusted market. Taking them in turn:

First, initiation - the pioneers, and then the first wave of pioneers, provide the first density of quality across startups. We knew this was happening in 2020, and it’s the reason a successful seed fund was possible then despite the difficulties of earlier efforts in the market.

Second comes Growth - this inflection happens when enough of the companies in the first wave hit scaling velocity with a product that is differentiated enough in the market, and when founders don’t sell out early. This enables true new players that either become standalone companies, or are purchased at revenue levels that were unlikely in the initiation phase, sparking the interest of other investors, entrepreneurs, and talent.

And once enough Growth companies emerge, while the top of the funnel of startups continues to build, feeding the growth stage, you get to a pattern where everybody agrees that the market is investable and everyone said they knew it was inevitable. That’s the maturity phase.

It always astounds me that we are going through this because we’ve been manipulating water, we’ve been water technologists for thousands of years. But only recently have we seen the emergence of water as a viable destination for capital at any kind of scale - and we still have a long way to go. But the critical mass of smart founders that we saw in 2020 has moved through the initiation stage and the growth stage is here. This is a crucial time for the development of any sector, as it’s when we see the first real exits on a venture timeline, the first recycling of capital and talent, back into other startups but also into the investment world. These first larger moves bring in interest from larger players, and also force interesting conversations for incumbents - do they accommodate, cooperate with, compete with or purchase the companies coming down the funnel?

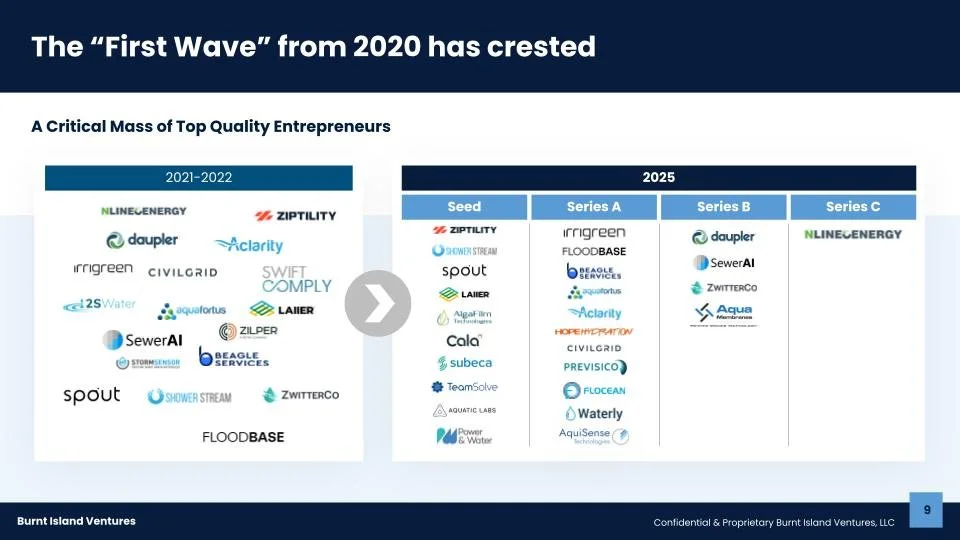

The box on the left is what we talk about when we say a critical mass of talent, and this excludes the EXCELLENT companies we said no to in this period of investment of our Fund I. We have always had talented people building businesses in water (and we have three exited founders on our team - one partner and two venture partners). But what was incontrovertibly true was that in 2020 there were suddenly enough of these founders such that you could make mistakes, of both omission and commission, and still have a margin of safety on being able to fund exceptional people in the deployment period of a Fund. These companies that we saw in 2020-2022 have now been joined by another 15 founders from our Seed Fund, starting in 2023, and Aqua Membranes from our Growth Fund.

And it’s working - our overall graduation rate will be 92%, and we have a 2% loss ratio on capital invested. Fund I companies will do $80m in revenue this year, $120m in bookings, and half of them are either already profitable or have a clear pathway to being so. Fund II’s companies will do $35m in revenue, and we’re only in year 2 of the Fund.

What you’re seeing is these smart people building the companies they said they would, moving through the fundraising stages, even though that’s sometimes a poor proxy for actual development.

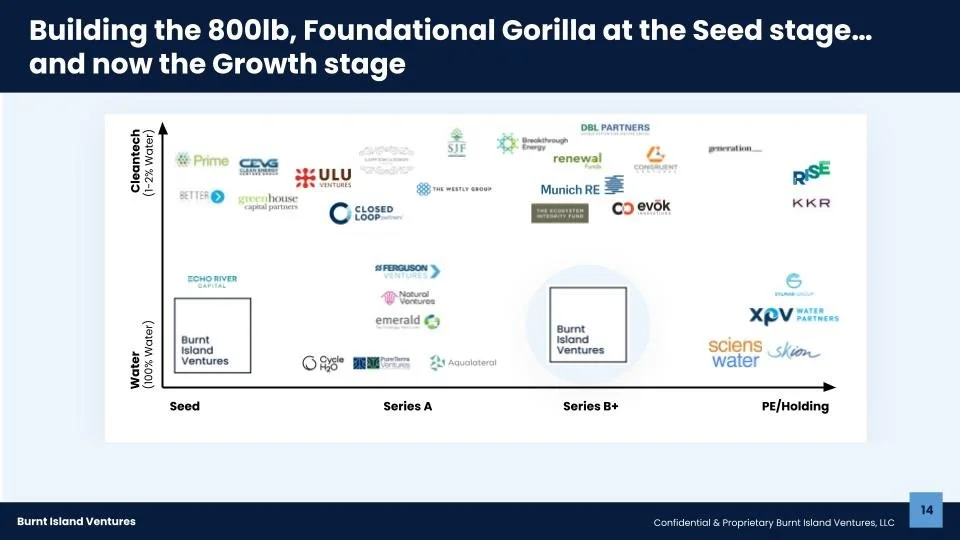

This is symptomatic of an overall trend in water which we believe is permanent. The smart people are here, more and more of them every year, and they’re building really good companies. I was lucky enough to start at Imagine H2O the water Accelerator in 2015, and work directly with many of the non-BIV names on this slide. But what’s crucial to note is that 5 years ago, that Series B box and most of that Series A box was empty. The smart people have built their companies into the early growth stages, and in a couple of instances beyond. This is literally what category creation looks like.

And the overall capital flows to water reflects the explosion of talent, and the quality of companies being built. 2023 investment was 4x that of 2020, which had a serious last couple of quarters in the overall venture industry, and 2023, 2024, 2025 will be well in excess of 2021, which was venture’s banner year since the dot com bubble. Notice the fattening of the Venture Growth and Late Stage VC slices. This is due the increasing number of companies moving through to the growth stage (though these numbers are skewed slightly by large individual deals, some of them not good ideas).

All markets need liquidity, so what happens with exits is a fundamental indicator of the maturity of a market. Deals at scale are vital to prove willingness to pay from the largest entities - and in the early stages of moving through the middle of the S-curve it doesn’t have to be startups that are bought. Platform purchases from PE and large moves from existing and emerging incumbents usually precede large startup exits. But now we’re seeing both. We predicted 3 $1bn+ deals in water in 2025, and we are at 8 and counting, excluding the American Water/Essential Utilities merger. There is a line around the block of PE firms looking to transact on both the buy and sell side. The data is crystal clear, here in the bottom right. Active deals are up 3.5x since 2020, and exits are up over 7 times. This pace will be maintained - PE has discovered the beauty of the water market, with its predictable, sticky revenues, good unit economics, tailwinds from both renewal and demand for new capacity across utility and industrial, and across the world. It’s just a great business to be in.

So what we have is growing companies running full steam ahead into the arms of pools of capital who are already sold on the sector. The only real question for the completion of the S-curve, moving to the steady state where this will mature as a destination for every flavor of venture and growth capital, is how fast it will take for co-investors to get it, and how big the specialists can get. And this slide illustrates this step is already derisked. We’re so proud to have invested alongside all these firms in companies that are working, and in most cases working really well. You will see our logo here twice - it’s not a big visual typo. We established ourselves at the Seed stage starting in 2020 predicated on the argument we have gone through here. The talented founders we saw in 2020 and 2021 have now to a large extent built the companies they said they would, and guess what? There is no water-focused growth fund, entering at the Series B or beyond. So we’re building it - $75m with a hard cap of $100m, we’re more than a third through it and we’re so excited to expand our investment activities following the maturation of the private investment market in water.

Because our job, in the context of the expectation of more mainstream competition, is to be the investor of choice for founders at the seed stage, and adding downstream capacity to stay with companies for longer AND have more flexibility in entry points in pursuit of multiples for our LPs will be a huge asset in the years to come.

This new phase in water financing has implications for all the players.

For Founders this is very good news. The deals for SmartCover, Urbint, Locusview, Consigli are just the start, and as the exit market gets clearer, your companies get more valuable. Enjoy. Just don’t raise your prices on us.

For Investors of all stripes - whether you’re public, private, bond, private credit, special situations, whatever it is, water is something you want exposure to now. This isn’t a funny appendage of the market, it’s foundational, most revenue drivers insulated from the business cycle, it’s going to mature rapidly, and it doesn’t pay to be late to the party.

Corporates - you’re going to have some decisions to make! The sleepy days of yesteryear where anyone who emerged from the Series A stage was both rare and affordable are gone. Then you could pay relatively little to take on an extra value proposition for your customers, or remove an emergent competitive threat. Now the landscape is more complicated. Not least because it is an increasingly target-rich environment for large companies who want to start playing in the sector. Really good startups are excellent wedge acquisitions, because they can’t get past a certain stage without being fundamentally differentiated - and owning that differentiation is valuable.

There are many elements of financing we have not covered, nothing on credit which will continue to emerge, and needs to, especially in working capital provision. Nothing on the bond markets, very little on public markets. That’s partly because I don’t work in those markets and it’s important to stick to your circle of competence, but it’s more because what you’re looking at here is the core of the development and maturation of all of those other verticals. Sectors need to have a thriving ecosystem of new companies, of talent and treasure recycled, of new companies finally getting really big in order for all the other areas of finance to be enabled. The beginning of the next wave means the finance environment in water is going to get rather interesting for an awful lot of people.

Thank you so much for listening, thank you so much to SWA for having me, and I look forward to connecting with you over the rest of the day.